ZDR

Conservative investment strategy has withstood crisis periods and is paying off

Although the results for 2022 have not yet been finalised, we already know that despite the worsening macroeconomic situation, we will be able to call the past year a record year. In this article, we provide a small recap related to the outlook for 2023, as well as a reflection on the factors that ultimately positively influence our investment strategy.

Looking back at 2022

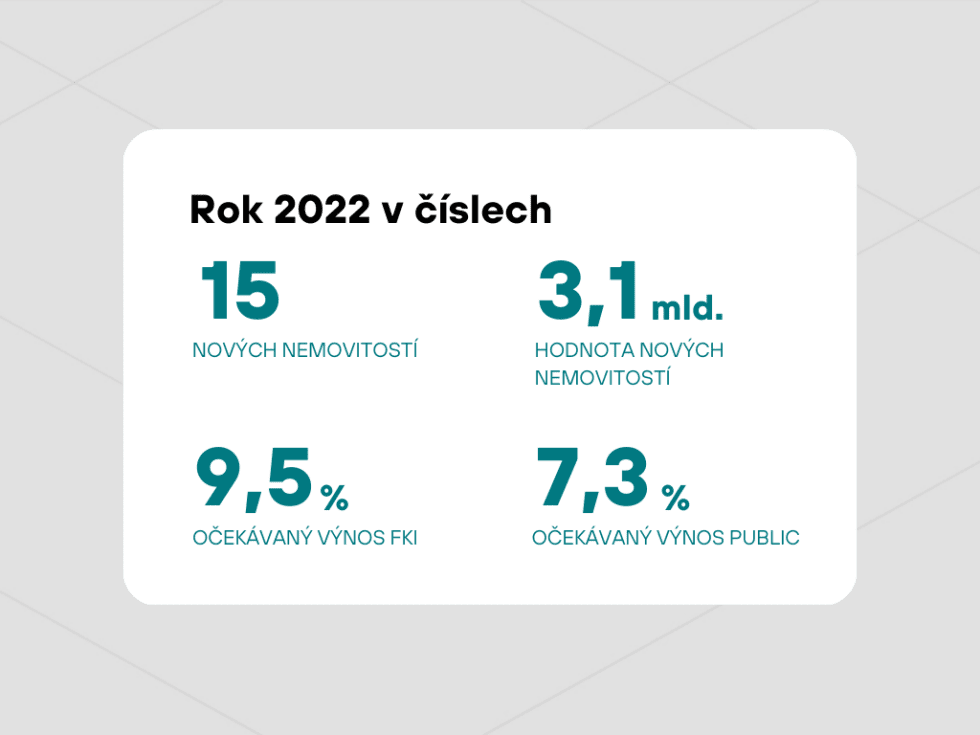

Despite the unfavourable situation on the markets, our funds did well last year, so we can say that their returns will reach an all-time high. We managed to add 15 new properties to our portfolio worth over 126 Mio euro, celebrated our five-year anniversary and launched a new fund, ZDR Industrial, which focuses on suburban logistics and manufacturing. Thanks to early investors who took advantage of the share subscription period, we bought the first property into the new fund before the end of the year.

The ambition for 2023 is to expand the portfolio for ZDR Industrial to include assets worth around half a billion CZK. Our main focus, however, remains on retail parks, which we know very well and are a proven working model for us and our investors through many crises.

A strategy that works in the world

Our strategy is based on investing in retail properties with tenants offering mainly groceries, other daily necessities or a lower-priced discount assortment. And it is the high proportion of food stores that sets us apart from the rest of the market. We can see that this approach works without major fluctuations outside the Czech Republic, where this strategy is even more widespread than here.

Among the foreign real estate funds that we follow and have a similar focus as ours, we can mention, for example, the Greenman fund. One of the largest retail investors in Germany with a portfolio worth a billion euros, which is double ours by comparison. From the available data, it is clear that this fund has an even higher percentage of food retailers in its lettable space than we do. It is as high as 63%. Their annual appreciation is consistently around 5%.

What is particularly important about this example is that even in times of decline in traditional asset classes, investments in real estate of our type still retain value. Despite the many differences, there is one common denominator, and that is stability and conservatism.

Property price corrections - what do we need to consider?

Recently, there has been more and more talk of falling property prices. But here again, real estate funds are proving to be a reliable and long-term store of value. It is essential to distinguish what type of property is involved, what its condition is, where it is located and what tenants occupy it.

In recent years, prices of apartments and logistics halls in particular have risen sharply. These assets may therefore be more susceptible to price declines. Retail parks, which are our focus, have of course also risen in price, but gradually and at a natural pace. Taking into account the above-average length of our leases (WAULT 6.3 years), the creditworthiness of our tenants and the regular rent increases due to indexation, we expect stagnation in this segment at worst.

For comparison, we can again look abroad. Let's look at Vienna, where we have our assets and where we know the market. The difference in the price of apartments between Vienna and Prague is 17%. Given that the average income of Viennese residents is more than 60% higher than that of Prague residents, apartments in Prague are already significantly more expensive. The average gross rental yield in our capital city is 2.62%. As far as generating a return is concerned, at the current level of interest rates, and after taking into account operating costs, it does not make much sense to acquire an investment apartment.

The situation is different for retail parks. The historical development of their prices has been rather gradual but consistent compared to other types of commercial real estate. The market valuation of Czech retail parks is at the level of 6-7%. Compared to Austria, specifically again to Vienna, we are still 30% lower in terms of valuation.

The general trend is a shift in prices towards the west, i.e. upwards. Therefore, we see a much higher growth potential here than is currently offered by, for example, the above-mentioned apartments. Furthermore, we are betting on our proven defensive strategy and do not expect any negative developments in the performance of our funds in the near term.

Strategie, která funguje i ve světě

Naše strategie je založená na investování do maloobchodních nemovitostí s nájemci nabízejícími převážně potraviny, další zboží denní potřeby nebo levnější sortiment diskontního charakteru. A právě vysoký podíl prodejen potravin je něco, co nás odlišuje od zbytku trhu. To, že tento přístup bez větších výkyvů funguje, vidíme i mimo Českou republiku, kde je tato strategie dokonce rozšířenější než u nás.

Ze zahraničních realitních fondů, které sledujeme a mají podobné zaměření jako my, můžeme jmenovat například fond Greenman. Jednoho z největších retailových investorů v Německu s portfoliem v hodnotě miliardy eur, což je pro srovnání dvojnásobek toho našeho. Z dostupných údajů je zřejmé, že tento fond má dokonce vyšší procentuální zastoupení potravinářů na pronajímatelných plochách než my. Uvádí až 63 %. Jejich roční zhodnocení se konzistentně pohybuje kolem 5 %.

Důležité na tomto příkladu je zejména to, že i v době propadu tradičních tříd aktiv si investice do nemovitostí našeho typu stále udržují hodnotu. Přes mnohé rozdíly zde existuje jeden společný jmenovatel a tím je stabilita a konzervativní charakter.

Korekce cen nemovitostí – co je potřeba vzít v potaz?

V poslední době se stále více hovoří o poklesu cen nemovitostí. I zde se ale ukazuje, že realitní fondy jsou spolehlivým a dlouhodobým uchovatelem hodnoty. Je nezbytné rozlišovat, o jaký typ nemovitostí se jedná, jaký je jejich stav, kde se nachází a jakými nájemci jsou obsazené.

Během posledních let prudce rostly zejména ceny bytů a logistických hal. Tato aktiva tedy mohou být náchylnější na pokles ceny. Retailové parky, na které se soustředíme, samozřejmě na ceně rostly také, ale postupně a přirozeným tempem. Přihlédneme-li k nadprůměrné délce našich nájemních smluv (WAULT 6,3 let), bonitě nájemců a pravidelnému navyšování nájemného vlivem indexace, očekáváme v tomto segmentu v horším případě stagnaci.

Pro srovnání se opět můžeme podívat do zahraničí. Vezměme si pro názornost Vídeň, kde máme naše aktiva a tamní trh známe. Rozdíl v ceně bytů je mezi Vídní a Prahou 17 %. S ohledem na fakt, že průměrný příjem obyvatel Vídně je o více než 60 % vyšší než Pražanů, vychází byty v Praze už podstatně dráž. Průměrný hrubý nájemní yield je v našem hlavním městě 2,62 %. Pokud nám jde o generování výnosu, tak při současné úrovni úrokových sazeb, a po započtení provozních nákladů, nedává pořízení investičního bytu příliš smysl.

U retail parků je situace odlišná. Historický vývoj jejich cen byl v porovnání s jinými typy komerčních nemovitostí spíše pozvolný, zato konzistentní. Tržní ocenění českých retail parků se pohybuje na úrovní 6-7 %. V porovnání s Rakouskem, konkrétně třeba opět s Vídní, jsme z pohledu ocenění stále o 30 % níže.

Obecným trendem je posun v cenách směrem k západu, tedy nahoru. Proto zde vidíme podstatně vyšší potenciál růstu, než aktuálně nabízí třeba výše zmíněné byty. Dále sázíme na naši osvědčenou defenzivní strategii a v nejbližším období neočekáváme negativní vývoj u výkonnosti našich fondů.

.jpeg)

Label

Let your capital work for you in real estate across Europe

1

Leave us a contact

2

We’ll get in touch and guide you through the steps

3

Start earning with your investment

We will contact you as soon as possible and together we will select the best way to invest.